Solid-State EV Batteries Are Still Two Years Away — and Have Been for a Decade. Here's What's Actually Different Now.

The Promise That Won't Quit

Solid-state batteries have been "two years away" since at least 2014. The promise is compelling: higher energy density, no flammable liquid electrolyte, faster charging, longer cycle life. That promise has driven tens of billions in investment from Toyota, Volkswagen, Samsung, and the U.S. Department of Energy. In 2025-2026, something actually changed: Toyota completed road testing of a solid-state-equipped Lexus RZ prototype, Samsung SDI and QuantumScape hit key production milestones, and the engineering challenges have narrowed from "fundamentally unsolved" to "manufacturing at scale." Here's an honest assessment of where things stand.

What Makes Solid-State Different

Current lithium-ion batteries use a liquid electrolyte — a lithium salt dissolved in an organic solvent — to shuttle lithium ions between anode and cathode. That liquid is flammable, which is why EV fires burn so intensely. It's also why Tesla, GM, and others spend heavily on thermal management systems.

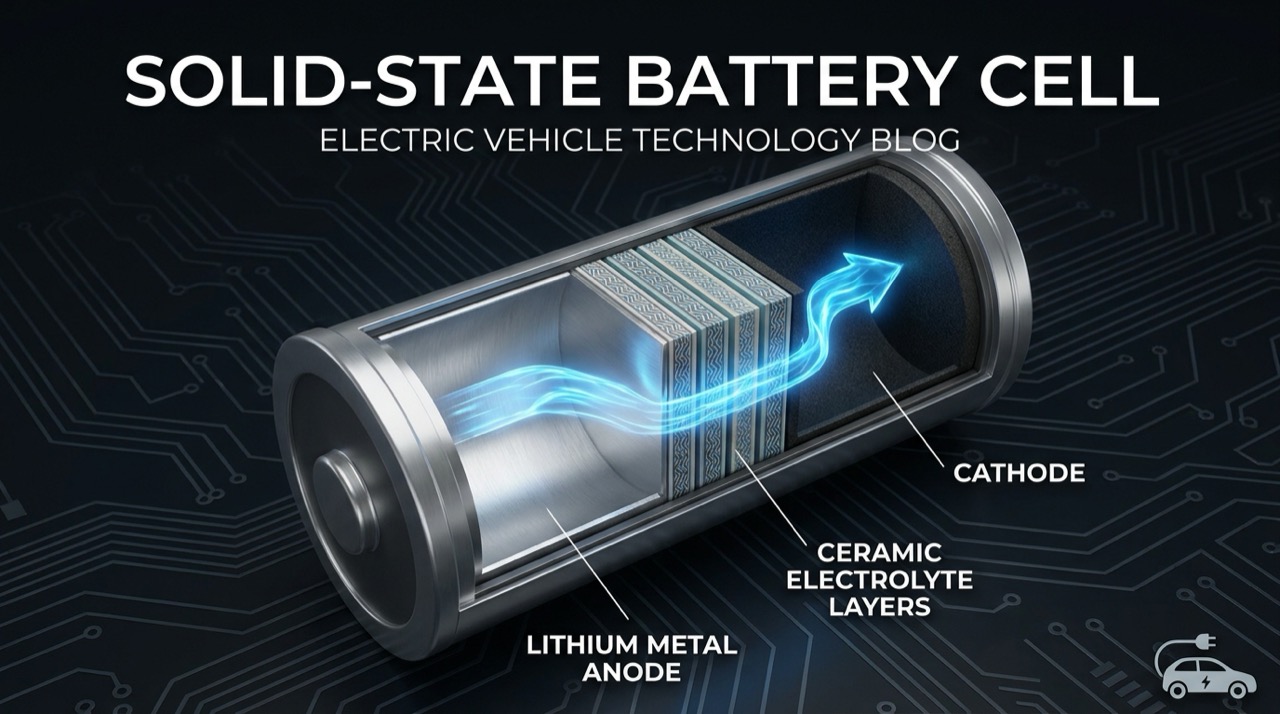

Solid-state replaces the liquid electrolyte with a solid ionic conductor. Three main approaches exist:

- Oxide ceramics (e.g., LLZO — lithium lanthanum zirconium oxide): stable, non-flammable, but hard to manufacture thinly and has high interface resistance.

- Sulfide electrolytes: better ionic conductivity, but react with moisture — requiring dry-room manufacturing more demanding than current lithium-ion.

- Polymers: easiest to manufacture but typically only work at elevated temperatures, limiting practical application.

The key benefit: solid electrolytes allow a lithium metal anode instead of the graphite anodes in today's cells. Lithium metal stores roughly 10 times more lithium per gram than graphite. Combined with a solid electrolyte that tolerates higher voltages, energy density jumps dramatically.

Current best lithium-ion cells achieve around 300 Wh/kg. Solid-state targets 400-500 Wh/kg. At 500 Wh/kg, a Tesla Model 3's 82 kWh battery pack would provide approximately 600 miles of range at the same weight — or the same range in a pack weighing 40% less.

The Manufacturing Problem That Kept It "Two Years Away"

The classic failure mode: solid electrolytes crack. During charge and discharge cycles, the anode and cathode expand and contract — up to 300% volume change for a lithium metal anode. A liquid electrolyte accommodates this movement; a solid ceramic layer cracks, creating dead zones that degrade capacity.

Sulfide electrolytes have good ionic conductivity but react with atmospheric moisture to produce toxic hydrogen sulfide. Manufacturing at scale requires dry rooms with dew points below -40°C, significantly more demanding and expensive than conventional lithium-ion production.

Interface resistance is the third problem. Where a liquid electrolyte contacts an electrode, the interface is intimate — molecules fill every surface irregularity. Solid-to-solid interfaces have much higher resistance, reducing the practical current the cell can deliver and limiting fast-charge capability.

These aren't theoretical problems. They caused Toyota to delay production targets four times between 2018 and 2023. They caused QuantumScape to miss multiple milestones that were priced into its stock at the 2020 SPAC valuation.

What's Actually Different in 2025-2026

Toyota

Toyota began road testing a solid-state-equipped Lexus RZ prototype in 2024 — real vehicles on real roads, not just dynamometer testing. The company's internal target is limited production by 2027-2028. Their key breakthrough is a proprietary sulfide electrolyte formulation that remains stable under the compressive pressure applied during cell assembly and cycling, reducing the cracking problem significantly. Toyota claims 1,200 km range and 10-minute charging capability in lab conditions. Those numbers require context: lab conditions with optimized temperature and discharge rates. Real-world range will be lower. But the direction is correct.

QuantumScape

QuantumScape, backed by Volkswagen and early investor Bill Gates, shipped A-sample cells to automotive OEMs in 2024 for evaluation. Their design is anode-free: no graphite at all. Lithium metal plates directly onto the separator during charging — the anode forms in-situ. This eliminates a manufacturing step but makes cycle life dependent on how cleanly lithium plates and strips. In 2026, QuantumScape is at B-sample production stage at its pilot facility in San Jose, targeting 100,000 cells per year. That sounds like volume; automotive scale requires hundreds of millions of cells per year. They remain years from commercial scale.

Samsung SDI

Samsung SDI announced 2027 as its production target for solid-state cells destined for BMW vehicles. Their all-solid-state battery (ASSB) uses an oxide electrolyte — the more stable but harder-to-thin approach. Samsung SDI is targeting cells in the 900 Wh/L range, roughly double current energy density by volume. BMW's 2027 timeline is aggressive; most observers expect 2028-2029 for first limited deliveries.

Solid Power

Solid Power, backed by BMW and Ford, made a notable strategic pivot: they shifted from full solid-state to semi-solid (hybrid electrolyte) after pure solid-state proved too expensive to scale on their timeline. They are now targeting semi-solid cells for 2026 pilot production. This is a significant acknowledgment that pure solid-state at automotive cost targets remains out of reach for near-term production.

The Semi-Solid Middle Ground

Several companies have found that a hybrid approach — a predominantly solid electrolyte with a thin liquid layer retained at electrode interfaces — captures most of the safety and energy density benefits at significantly lower manufacturing cost. The interface resistance problem is reduced because the liquid layer handles contact with the electrode surface.

CATL's Condensed Battery, announced in 2023, claims 500 Wh/kg and uses what CATL describes as a "condensed state" electrolyte — effectively semi-solid. It entered limited production for COMAC aircraft use in 2024, making it the highest-energy-density cell in commercial production globally. BYD's next-generation blade battery reportedly targets semi-solid chemistry for 2026.

The pattern emerging: pure solid-state for consumer vehicles likely won't arrive until 2028-2030. Semi-solid is the 2026-2027 bridge technology that delivers meaningful density and safety improvements without requiring the full manufacturing revolution that pure solid-state demands.

What It Means for EV Buyers

Solid-state and semi-solid cells will enter vehicles at the premium end first — expect $80,000+ vehicles in 2027-2028 to be the initial application, where the cost premium is absorbable. Mass market adoption follows the usual 5-7 year trickle-down.

The more immediate impact for buyers in 2026: today's best liquid-electrolyte cells are very good and improving fast. CATL's Qilin battery (NMC chemistry, liquid electrolyte) achieves 255 Wh/kg with 10-minute fast charge capability. BYD's blade battery offers outstanding cycle life and safety at lower energy density. The gap between today's best liquid-electrolyte cells and tomorrow's solid-state is narrowing even as solid-state improves — the incumbent technology isn't standing still.

The China Factor

CATL and BYD together control approximately 57% of global EV battery supply. China's government has directed over $1.5 billion in targeted R&D grants to solid-state battery development since 2020, with CATL, BYD, SVOLT, and CALB all receiving funding. CATL has publicly targeted solid-state commercial production in 2027.

If CATL achieves solid-state at automotive scale before Toyota or QuantumScape — and they have manufacturing scale advantages that Western startups cannot match — the competitive implications for Western automakers are severe. A CATL solid-state cell at 450 Wh/kg in a $40,000 vehicle by 2029 would reset competitive dynamics industry-wide.

The Honest Bottom Line

Solid-state batteries are no longer vaporware. Specific companies have working cells that have been tested in real vehicles and evaluated by automotive OEMs. The manufacturing challenges are engineering problems — yield rates, interface stability, moisture control, cost per kWh — not fundamental physics barriers. That distinction matters.

But "two years away" translates to 2027-2028 for first limited production vehicles and 2030 or later for meaningful mass-market volume. The supply chain for solid-state electrolyte materials doesn't exist at scale. Dry-room manufacturing capacity needs to be built. Cell-to-pack integration for solid-state requires different mechanical designs than liquid-electrolyte packs.

For EV buyers in 2026: the best available lithium-ion vehicle is the right purchase today. Solid-state will define the next generation of EVs, not this one. Watch for semi-solid cells in premium vehicles by 2027-2028 as the leading indicator that the technology is genuinely arriving — and watch CATL's production announcements as closely as Toyota's and QuantumScape's.