The GLP-1 Revolution: How Ozempic and Wegovy Are Reshaping Medicine Beyond Weight Loss

Semaglutide was first approved by the FDA in 2017 under the brand name Ozempic, for type 2 diabetes management. The drug worked — better than most existing options — but so had other diabetes drugs, and the field had seen plenty of incremental improvements. Nobody predicted that the same molecule, at a higher dose and sold as Wegovy, would touch off a pharmaceutical revolution that's still accelerating in 2026.

The scale of the shift is difficult to overstate. Novo Nordisk briefly became the most valuable company in Europe in 2023 on the strength of semaglutide sales alone. Eli Lilly's tirzepatide (Mounjaro, Zepbound) produced weight loss results in trials that surpassed every previous pharmacological intervention. The cardiovascular, neurological, and addiction-related findings emerging from large-scale trials have expanded the potential patient population from the obese to nearly anyone with metabolic risk factors — a market that encompasses hundreds of millions of people.

What GLP-1 Agonists Actually Do

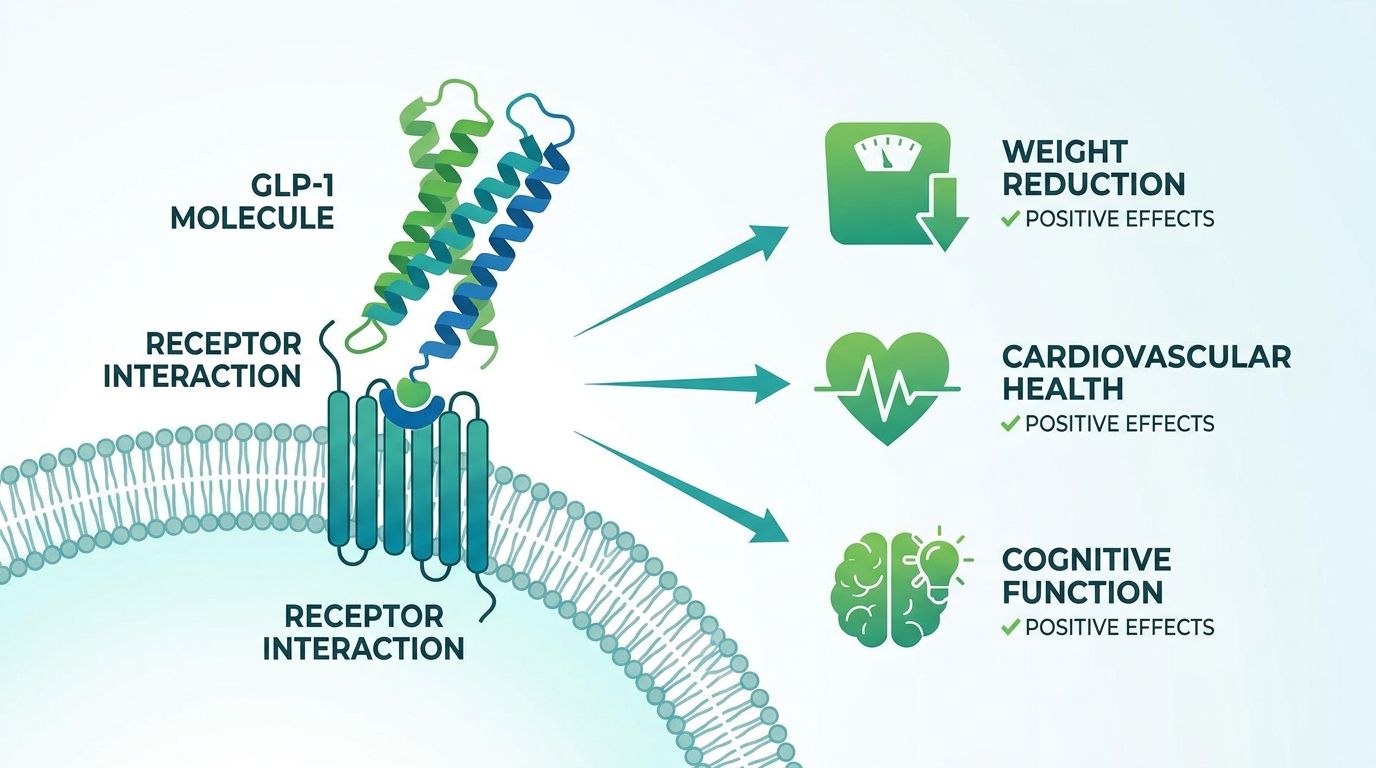

Glucagon-like peptide-1 is a hormone produced in the gut in response to food intake. It signals the pancreas to release insulin, slows gastric emptying (so food is absorbed more gradually), and — crucially — acts on receptors in the brain, particularly in the hypothalamus and reward centers, to reduce appetite and food-seeking behavior. GLP-1 receptor agonists are synthetic versions of this hormone, engineered to have a longer half-life than natural GLP-1 (which is degraded within minutes).

The mechanism is not simply appetite suppression. Early descriptions of GLP-1 drugs as "making food less interesting" understated the scope. The drugs appear to modulate reward circuitry in ways that reduce the motivational pull toward highly palatable foods specifically, rather than hunger in general. This is why clinical trial participants often report that food thoughts that previously occupied significant mental bandwidth simply become quieter — a qualitative change in relationship to eating, not just reduced calorie intake through willpower.

Beyond Obesity: The Cardiovascular Signal

The SELECT trial, whose results were published in 2023, was not a weight loss study. It enrolled 17,604 overweight or obese adults with established cardiovascular disease but no diabetes history, and randomized them to semaglutide or placebo. The primary endpoint was major adverse cardiovascular events — heart attack, stroke, cardiovascular death. Semaglutide reduced that composite endpoint by 20% over three years.

This is a large effect. For context, statins — the standard of care for cardiovascular risk reduction — typically reduce major adverse cardiovascular events by 25–35% in high-risk populations, but they've been in use for 40 years and their effect is understood mechanistically through LDL reduction. The SELECT result suggests GLP-1 agonists have cardiovascular benefits that extend beyond weight loss (participants lost a median of ~9% of body weight, but the cardiovascular benefit appeared early — before weight loss was substantial — suggesting independent mechanisms).

The FDA approved semaglutide for cardiovascular risk reduction in people with established cardiovascular disease and overweight/obesity in March 2024, expanding the indication well beyond metabolic disease management.

The Addiction Finding

Among the more unexpected findings: patients taking GLP-1 agonists have reported reductions in alcohol consumption, smoking, and other addictive behaviors. This observation was initially anecdotal — patients mentioning to their physicians that they were drinking less or had lost interest in cigarettes — but has been supported by multiple clinical observations and animal studies.

The mechanism appears to involve the same reward circuitry the drugs affect for food. GLP-1 receptors are expressed in the nucleus accumbens and ventral tegmental area — core components of the dopaminergic reward system — and agonism at these receptors appears to blunt the reinforcing effects of alcohol and potentially other substances. Randomized trials testing GLP-1 agonists specifically for alcohol use disorder are underway, with preliminary results expected in 2026–2027. Several smaller studies have already shown statistically significant reductions in alcohol consumption and craving scores.

If these signals survive larger-scale trials, the implications are significant. Effective pharmacological treatments for alcohol use disorder are limited — naltrexone and acamprosate have modest efficacy and poor adherence. A drug that addresses metabolic disease, cardiovascular risk, and substance use disorder simultaneously would represent a qualitative change in treatment capacity for conditions that together affect hundreds of millions of people.

Manufacturing Constraints and Access Inequity

The gap between clinical benefit and real-world access is stark. As of mid-2026, demand for GLP-1 agonists substantially exceeds manufacturing capacity. Novo Nordisk and Eli Lilly have invested billions in new production facilities — peptide synthesis at this scale requires specialized fill-finish manufacturing infrastructure — but supply shortfalls have persisted for over two years.

The cost compounds the access problem. Wegovy lists at approximately $1,350 per month in the United States without insurance coverage. Medicare only recently began covering GLP-1 drugs for cardiovascular risk reduction following the SELECT trial results; coverage for obesity alone remains patchy across plans. In countries with negotiated national pricing — the UK, Germany, France — costs are substantially lower, but availability constraints still limit access.

The equity dimension is significant: clinical trials have enrolled populations that skew white and affluent, and the patients most affected by obesity-related metabolic disease — lower-income and minority populations with higher rates of food insecurity and limited healthcare access — are those with the least access to the treatments that would benefit them most. Compounded semaglutide (cheaper, unbranded versions prepared by compounding pharmacies) has partially filled the gap in the US, but its quality consistency and regulatory status remain contested.

What's Coming Next

The pipeline is accelerating. Eli Lilly's oral retatrutide — a triple agonist hitting GLP-1, GIP, and glucagon receptors — produced 24.2% average weight loss in phase 2 trials, approaching the results of bariatric surgery. Novo Nordisk's CagriSema (semaglutide + cagrilintide) showed 25.1% weight loss in a 68-week trial, also approaching surgical outcomes pharmacologically.

Oral formulations are in advanced trials, which would transform delivery from weekly self-injection to daily pill — significantly expanding the addressable population (many patients decline injectable therapies). The costs of manufacturing oral small-molecule GLP-1 agonists are also lower than peptide injectables, which may eventually address affordability.

The emerging research frontier is neurological. GLP-1 receptors are expressed in the brain in regions associated with neuroinflammation and neurodegeneration. Observational studies have found reduced rates of Parkinson's disease and Alzheimer's disease among patients taking GLP-1 agonists for diabetes. Randomized trials specifically targeting these conditions are now running, with results expected over the next three to five years. If the neurological signals prove robust, the drug class may expand beyond the already-large metabolic and cardiovascular indications into neurodegeneration — a target that has resisted pharmacological intervention for decades.